With over 40 years experience in all facets of Retirement Plans, we have the knowlege and insight to guide Plan Sponsors and Individuals to their GOALS.

Institutions

Fiduciary Guidance So Retirmement Plan Sponsors Are Confident In Their Decisions.

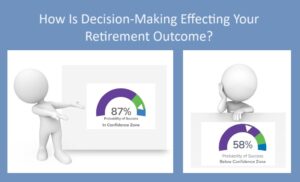

“75 percent of Americans are ‘winging it’ when it comes to their financial future.”

CNBC Survey, August 2019

Why Choose Us

WE ARE FIDUCIARIES! That means we work for our clients and their best interest. Did you know not all Financial Professionals are held to the same standard? In fact only about 25% are Fiduciaries.

Our approach begins with getting to know you and your goals. No sales pitches. No pressure.

Play Video

Chip discusses his “WHY” in this short video.

Get In Touch

We would love to hear what is on your mind. Schedule a meeting using the calendar.